When a Nork Missile Launch is Not a Nork Missile Launch

Can a prediction market fail to predict even the past? One of the more vexed issues for prediction markets is defining the terms of their contracts. Intrade’s North Korean missile launch contract has continued to trade, because the US DoD has not officially confirmed that the missiles left North Korean airspace (12 nautical miles from the coast), as per the terms of the contract. NorCom will only say the missiles landed in the Sea of Japan.

In absence of such confirmation, Intrade will expire the contract at zero, even if more missiles are launched. The price action in the contract thus probably tells us more about the confusion over the terms of the contract and the willingness of the DoD to divulge additional information than it does about the prospects for missile launches. It also provides a nice illustration of the role of asymmetrical information in markets, given the willingness of some to short the contract in the immediate aftermath of the missile launches, with volume exceeding what would be expected from the squaring up of long positions placed in advance of the launches. See the discussion at the TEN Forum (via Chris Masse).

UPDATE (17 July): More on the North Korean missile launch that wasn’t, from Intrade:

Dublin, July 17, 2006: North Korea Missile Test Exchange News Update

The Exchange confirms that it has sought direct confirmation from the US Department of Defense regarding the above contract.

As of today’s date no such confirmation has been received.

As is standard operating procedure to ensure orderly operation and expiry of all markets, the Exchange is and will remain proactive in looking for verifiable settlement related information from the relevant authority.

The Exchange will not use third party non-verifiable confirmations for settlement of any contract.

posted on 10 July 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Why Glenn Stevens Will Enjoy a Smoother Transition than Ben Bernanke

Ian Macfarlane’s current three year term as RBA Governor ends in September. The SMH profiles his likely successor, Deputy Governor Glenn Stevens:

Your mortgage may soon be in the hands of a guitar-playing amateur pilot from Sylvania Waters.

Glenn Stevens is likely to enjoy a much smoother transition than Ben Bernanke. An incredible amount of nonsense was written about Bernanke as he moved into his role as Fed Chairman and markets are probably still less than fully sold on his inflation-fighting credentials. This is a reflection of the weakness of the institutional framework for monetary policy in the US and Alan Greenspan’s promotion of a highly discretionary approach to policy he euphemistically termed ‘risk management.’ It is hardly surprising then that markets view the Fed’s inflation-fighting credentials as being only as good as the next Fed Chairman.

I would be surprised if anyone were to raise similar questions about Stevens. The key difference is the RBA’s commitment to an inflation targeting regime. As it happens, the RBA’s inflation targeting framework is only very loosely defined and the associated governance framework remains thoroughly antiquated. The RBA makes up for this, however, by having articulated the relationship between policy and its inflation target. The RBA’s approach to policy is now reasonably well understood, in a way that Fed policy arguably isn’t. The RBA’s experience shows that even the most basic commitment to an inflation target can give a central bank credibility that doesn’t just walk out the door when the central bank head leaves.

Glenn Stevens will be speaking on The Conduct of Monetary Policy on Thursday. Should be an interesting speech.

posted on 08 July 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

RBA Rate Hike Probabilities

Taking a leaf from David Altig’s regular updates of Fed funds rate probabilities, below we show the probability of a 25 bp RBA rate hike at each of the monthly post-Board meeting announcement windows.

Probabilities are derived from 30 day interbank futures. These are not as liquid as 90 day bank bill futures, so bid prices are sometimes substituted for last trade prices. Only contracts for which there is currently open interest are shown. Although it is common to estimate implied probabilities from bill futures, interbank futures have the advantage of being a monthly rather than quarterly contract and there is no need to make assumptions about the (variable) premium of 90 day bill yields over the official cash rate.

Note that the RBA has no regularly scheduled meeting in January. The probability for January is based on an unscheduled ‘inter-meeting’ move on the first Wednesday of January.

posted on 06 July 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

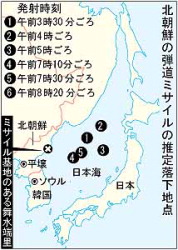

North Korean Missile Launches for Fun and Profit II

Intrade’s North Korean missile launch contract is still trading, well after confirmation that the Norks launched at least six missiles, including a long-range Taepodong 2 that failed 40 seconds after launch. It is not clear whether Intrade are waiting for confirmation that the missiles did leave North Korean airspace, as per the contract, or are just asleep because of the 4 July holiday in the US. It could be that the post-launch trades will actually be unwound, back to the time of the first newswire reports of the missile launches. Price action below:

UPDATE: The Mainichi plots where the missiles landed:

posted on 05 July 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Take Out the Black Helicopters and You’ve Got Bill Gross

Caroline Baum’s Just What I Said, a collection of her Bloomberg columns from the late 1990s through to the early 2000s, contains a chapter on financial market conspiracy theories. She also reproduces some of the correspondence she received in response to these columns:

Do you really believe the US dollar is worth anything? Print what you want but look in the mirror if you want to see a “truly duped” conspirator! The black helicopter you hear…it is coming for you Caroline.

Take out the black helicopter references and you’ve almost got Bill Gross.

At least some of Baum’s mailbag would appear to be tongue-in-cheek, but you can never be entirely sure:

Yes, Caroline, there are black helicopters and the day of pecuniary recompense for the filthy idolaters of usury is at hand. Right now, even as I type, the reptilian mercenaries from Cygnet 61 and Zeta Reticuli are emerging from their base camps to lay siege to the money houses of Wall Street…Soon, you’ll start to notice iguana-like chalky stool droppings in banks and financial offices all over Wall Street. That is the sign it’s time to get out of town and head for the nearest subterranean shelter.

posted on 30 June 2006 by skirchner in Economics, Financial Markets

(1) Comments | Permalink | Main

‘Excess Liquidity’ and Asset Prices

The always sensible Stephen Jen tries to give his colleagues an education on so-called ‘excess liquidity’ and asset prices:

What fraction of the financial activities (hedge funds’ long positions in risky assets, carry trades, etc.) is financed through bank credit? I suspect that many analysts have put too much emphasis on the outdated concept of monetary aggregates driving asset prices. It is the yield curve — the opportunity cost of liquidity — that is key, in my view, in thinking about asset prices. Since central banks no longer have a great influence on the yield curves, it is perhaps not correct to blame the central banks for high asset prices. So much of the financial activities are not a function of what banks do, but the non-bank financial institutions such as hedge funds. The monetary aggregates say nothing about what these institutions are up to, what their perceived risk is, and what their risk taking appetite is.

Further, the Marshallian-k analysis actually says that the US base money to nominal GDP ratio has declined over the past decade, and the broad money to nominal GDP ratio being flat for the past few years. Those who believe there is a positive link between the Marshallian-k and asset prices have to explain away these facts. Moreover, we need to be very careful about three concepts: interest rates, asset prices and the real economy. Clearly, they are all related, but the Marshallian-k says very little about asset prices, though it might have some implications for inflation.

I suspect that even in relation to inflation, most of the analysis based on conventional measures of ‘excess liquidity’ is mistaken. Given the largely demand-determined nature of monetary aggregates, what is commonly thought of as ‘excess’ liquidity is more likely to be an ‘excess’ demand for money, reflecting portfolio choices between money, other assets and spending that only indirectly reflect central bank policy actions.

UPDATE: David Miles makes a similar point:

shifts in the private sector’s desire to hold a part of its total wealth in a subset of assets labelled ‘money’ (bank deposits of various sorts) are many and varied. To a large extent they reflect portfolio movements that are driven by shifts in the perceived attractiveness of a very wide range of assets. Quite what the interpretation of a shift in broad money for spending and inflationary pressures should be is absolutely unclear, until you drill down to what is driving it.

posted on 29 June 2006 by skirchner in Economics, Financial Markets

(1) Comments | Permalink | Main

The Inflation Scare in Perspective

In the period since Bernanke’s appointment as Fed Chair, we have argued against the notion that Bernanke was somehow more dovish on inflation than his predecessor. Markets seem to have finally taken this in. Indeed, they now seem to be swinging in the other direction, with some very large hedge fund shorts in September eurodollar futures suggesting that some are looking for a 50 bp tightening from the Fed Thursday.

Alan Reynolds has a timely piece that puts the current inflation scare in perspective:

Others have expressed concern about “asset inflation” becoming embedded in core inflation. I cannot imagine how that idea ever gained credibility. The U.S. stock market boom of 1997-2000 was not followed by higher inflation. Neither was Japan’s land and stock boom of the late 1980s. Strength in asset prices in 1929 was perhaps the world’s worst predictor of inflation.

posted on 27 June 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

North Korean Missile Launches for Fun and Profit

Intrade has a contract available on a North Korean missile launch outside its airspace by 31 July, but not if Ashton Carter and William Perry get their way:

if North Korea persists in its launch preparations, the United States should immediately make clear its intention to strike and destroy the North Korean Taepodong missile before it can be launched. This could be accomplished, for example, by a cruise missile launched from a submarine carrying a high-explosive warhead. The blast would be similar to the one that killed terrorist leader Abu Musab al-Zarqawi in Iraq. But the effect on the Taepodong would be devastating. The multi-story, thin-skinned missile filled with high-energy fuel is itself explosive—the U.S. airstrike would puncture the missile and probably cause it to explode. The carefully engineered test bed for North Korea’s nascent nuclear missile force would be destroyed, and its attempt to retrogress to Cold War threats thwarted. There would be no damage to North Korea outside the immediate vicinity of the missile gantry.

posted on 22 June 2006 by skirchner in Financial Markets, Foreign Affairs & Defence

(0) Comments | Permalink | Main

Cranking Up the Wayback Machine on Stephen Roach

Stephen Roach accuses central banks of promoting ‘bubbles’ through excessively accommodative monetary policies. So I thought I would dig up what Roach had to say at the time of the last Fed easing in 2003 (emphasis added):

the key objective for the authorities is to get the US economy back to a sustainable 4% growth pace - and hold it there for several years. That’s the only way the deflationary gap between aggregate supply and demand can be closed once and for all. A temporary growth spurt won’t do the trick, and yet that’s a classic symptom of a post-bubble economy. I continue to fear that a post-bubble US economy plagued by a lack of policy traction will be unable to complete the critical transition from subpar to rapid growth. And that underscores the ultimate risk: A persistence of subpar growth in the current climate could take the US economy further down the slippery slope toward outright deflation.

Once again, financial markets are telling me that I’m dead wrong. The sharp run up in equities speaks of expectations of a sustained upturn in earnings that only a vigorous economy could deliver. The recent sharp sell-off in Treasuries speaks of a bond market that now believes that the Fed has done enough to fight deflation and spark a snapback in the real economy.

Yet, if I’m even close to being right on the economy, the markets could well be blindsided by the next in a long string of relapses.

That’s the problem with Roach: you are either in a ‘bubble’ or a ‘post-bubble.’ The ‘bubble’ paradigm is an all-purpose analytical framework that explains everything and nothing.

posted on 18 June 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Permabears Seek Validation in the Cycle

Markets are sending very strong signals of late. The yield curve inversion in the US and elsewhere, falling stock and commodity prices are all pointing to a weaker global growth outlook. The curve flattening in particular reflects a ‘stagflation trade’ which anticipates central banks overdoing monetary policy tightening to contain inflation pressures.

The permabears have been busy recasting their long-running structural bear call into a cyclical one, hoping the cycle will finally validate them. It is increasingly likely that the cycle will finally oblige them on at least some counts. If nothing else, they have the law of averages on their side. Yet markets have not yet delivered much joy to the purveyors of macroeconomic anti-Americanism. Just ask anyone who followed their advice and bought non-USD denominated asset markets, particularly Asian equities, as a hedge against USD weakness. So far, the USD has been a beneficiary of recent market developments and Asian equities have been crunched. Some hedge!

posted on 14 June 2006 by skirchner in Economics, Financial Markets

(7) Comments | Permalink | Main

The Wisdom of Crowds and Insider Trading

Henry Manne argues that the success of prediction markets supports the legalisation of insider trading:

The implications of what we already know of this “wisdom of crowds” approach to price formation, as against the traditional marginal pricing/arbitrage approach, are apt to be startling. We should rethink any current policies based on a view of pricing in which we exclude the best-informed traders and discard the wisdom of the many. For instance, we now have a new and more powerful argument than we had in the past for legalizing most insider or informed trading.

Since such trading clearly makes the market process work more efficiently, it aids capital allocation decisions and informs business executives through market-price feedback of the best predictions about the value of new plans. Furthermore, the Supreme Court’s “fraud on the market” theory of civil liability under the federal securities laws and Congress’s ideas of correct civil damage claims for insider trading no longer have any intellectual merit. The same is true of any other part of our securities laws implicitly based on the notion of the marginal trader as a rational arbitrageur of price.

The new approach would suggest that it is undesirable to have laws discouraging stock trading by anyone who has any knowledge relevant to the valuation of a security.

posted on 13 June 2006 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Page 45 of 45 pages ‹ First < 43 44 45

|