2010 01

Financial market economists are unanimous in expecting a 25 bp tightening from the RBA at Tuesday’s Board meeting, according to a Reuters poll taken today. February inter-bank futures are giving a 69% probability to a 25 bp tightening, while iPredict has an implied probability of 87%. Markets seem to be underpricing a tightening relative to the punditocracy, perhaps reflecting the same concerns driving weakness in equity markets.

posted on 29 January 2010 by skirchner in Economics, Financial Markets, Monetary Policy

(2) Comments | Permalink | Main

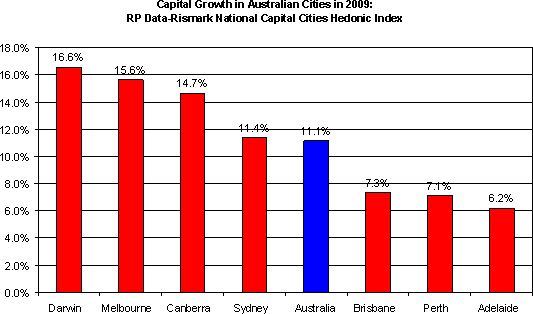

The RP Data-Rismark national capital city hedonic home price index for December shows a modest fall of 0.3% for the month, but up 2.1% for the quarter and 11.1% for the calendar year. This follows modest declines of 2-3% in 2008, which was the worst performance in history on this measure.

posted on 29 January 2010 by skirchner in Economics, House Prices

(0) Comments | Permalink | Main

From today’s Reserve Bank of New Zealand intra-quarter policy review:

As growth becomes self sustaining, fiscal consolidation would help reduce the work that monetary policy might otherwise need to do.

This is more the RBA’s style (see if you can guess when the RBA said it before clicking here):

The purpose of my answer was to explain why it was wrong to claim that rises in interest rates were due to the stance of fiscal policy.

My answer in no way constituted an attack on the Government’s fiscal policy.

Governor Macfarlane was right to argue that fiscal policy was then irrelevant to inflation and interest rates. But more recently, Governor Stevens has argued that fiscal stimulus has supported economic activity and that there is a trade-off between monetary and fiscal stimulus. Just don’t expect him to spell out the implications of that logic in a policy announcement as candid as that from the RBNZ.

posted on 28 January 2010 by skirchner in Economics, Financial Markets, Fiscal Policy, Monetary Policy

(0) Comments | Permalink | Main

Fama and French discuss the relative merits of TIPS versus cash as inflation hedges. Cash is an effective inflation hedge because short-term interest rates offer compensation for actual and expected inflation, with very low risk. As French notes:

Because the one-month T-bill rate changes to accommodate changes in expected inflation, unexpected inflation does not have the compounding effect that it has with longer-term bonds.

Of course, this assumes that short-term interest rates remain market-determined rather than set by regulation.

posted on 27 January 2010 by skirchner in Economics, Financial Markets

(1) Comments | Permalink | Main

Americans are far from sold on fiscal stimulus:

A CNN/Opinion Research Corporation survey released Monday morning also indicates that 63 percent of the public thinks that projects in the plan were included for purely political reasons and will have no economic benefit, with 36 percent saying those projects will benefit the economy.

Twenty-one percent of people questioned in the poll say nearly all the money in the stimulus has been wasted, with 24 percent feeling that most money has been wasted and an additional 29 percent saying that about half has been wasted. Twenty-one percent say only a little has been wasted and 4 percent think that no stimulus dollars have been wasted.

posted on 26 January 2010 by skirchner in Economics, Fiscal Policy, Opinion Polls

(0) Comments | Permalink | Main

The December quarter CPI to be released on Wednesday is seen at 0.4% q/q and 2% y/y, according to Friday’s Reuters poll. This is somewhat higher than the 0.1% q/q and 1.7% y/y implied by the TD-MI inflation gauge.

The trimmed mean is seen at 0.6% q/q and a steady 3.2% y/y. The weighted median is seen at 0.6% q/q and 3.5% y/y, down from 3.8% y/y in the previous quarter. It is noteworthy that despite a near two percentage point increase in the unemployment rate, core inflation was not reduced to an annual rate consistent with the RBA’s 2-3% target range during the recent economic downturn.

posted on 25 January 2010 by skirchner in CPI, Economics, Financial Markets, Monetary Policy

(3) Comments | Permalink | Main

The January Westpac-Melbourne Institute Consumer Sentiment survey finds that 84% expect house prices to increase over the next 12 months, with 21% expecting gains of over 10%.

posted on 23 January 2010 by skirchner in Economics, House Prices

(14) Comments | Permalink | Main

RBA Board member Graham Kraehe highlights the capacity constraints driving monetary policy tightening:

Asked if there was a risk of too much policy tightening choking off recovery, Mr Kraehe said the focus should be on price rises rather than supporting demand.

“The risk is more to cost pressure and inflation than it is to the demand side,” he said.

“Our unemployment has clearly now peaked. We’ve got increasing and continuing demand for employment in the resources sector that will put pressure on wages,” said Mr Kraehe, who is also chairman of Bluescope Steel.

“As an economy, one of the issues for us will be our ability on the supply side, whether it be on housing or the labour market, to supply enough resources to be able to take some of the pressure off cost inflation. Wages is one thing, housing another,” Mr Kraehe said.

posted on 22 January 2010 by skirchner in Economics, Financial Markets, Monetary Policy

(3) Comments | Permalink | Main

I have an op-ed in today’s Australian on the subject of global imbalances, arguing that it is distortions to capital allocation that make current account ‘imbalances’ problematic:

China will need to liberalise its capital account and domestic financial markets, moving its economy away from forced saving and unproductive, state-driven investment to a more market-driven system of capital allocation.

In this respect, China and the US have more in common than many Americans would like to think.

The US government will also need to extricate itself from its disastrous politicisation of housing finance and its post-crisis role in the US financial system.

In this regard, the US congress is likely to prove just as resistant to change as the Chinese Communist Party.

A less distorted system of capital allocation in both China and the US would have resulted in the more efficient use of global saving than was evident in the run-up to the global financial crisis. But it is unlikely to make much difference to the forces of globalisation driving persistent global imbalances.

posted on 22 January 2010 by skirchner in Economics, Financial Markets

(3) Comments | Permalink | Main

Jim Hamilton points to his Phillips curve relation, which is forecasting deflation over the near-term. For the long-run, he suggests we should look to the fiscal theory of the price level:

The value of the new Federal Reserve liabilities ultimately will be determined by the long-term fiscal soundness of the U.S. government….Inflation is not something you should be afraid of for 2010. But what we need is a convincing commitment from the government to both near-term stimulus and longer-term fiscal responsibility in order to be assured that it’s not a concern over the next decade.

And that’s not what I’m seeing from the U.S. Congress.

Meanwhile, Thomas Frank contemplates an evil plot to stick it to the gold bugs: putting Fort Knox on eBay. Not that it would work, but there is a certain irony in those who fear inflation taking refuge in the one real asset that is potentially the most vulnerable to a surge in supply from central banks and governments.

posted on 21 January 2010 by skirchner in Economics, Financial Markets, Fiscal Policy, Gold, Monetary Policy

(1) Comments | Permalink | Main

The federal government often references IMF reports in support of its policies, but is none too keen on facilitating interactions between Fund staff and the media. The IMF’s Independent Evaluation Office report on interactions with Fund members notes that:

the authorities of some advanced economies that had been major proponents of the Fund’s transparency policy in practice resisted the timely disclosure and dissemination of mission findings.

That would be us:

Press conferences/calls associated with the publication of the Public Information Notice and the Staff Report took place in the remaining countries, with the exceptions of Australia and New Zealand.

More from David Uren.

posted on 21 January 2010 by skirchner in Economics, Financial Markets, Media

(0) Comments | Permalink | Main

Australia maintains its third place in the Heritage Foundation-Wall Street Journal Index of Economic Freedom for 2010, once again trailing Hong Kong and Singapore. The US crash-dives to 8th place, behind Canada.

The index does not purport to measure political freedom. Australia’s political institutions are at least as free as any other country, and certainly more free than those in Hong Kong and Singapore. Australia could thus make a plausible case for being the world’s freest country after giving sufficient weight to the political as well as the economic dimensions of freedom, at least as measured by Heritage.

CIS will be holding an event on ‘Valuing and Measuring Economic Freedom’ on 28 January at which I will be speaking. Details here.

posted on 20 January 2010 by skirchner in Economics

(0) Comments | Permalink | Main

I have a column in today’s Business Spectator arguing that the global debate about whether monetary and fiscal stimulus will prove inflationary reflects poorly on the credibility of policymakers. One of the lasting effects of the discretionary policy responses to the global financial crisis may be the damage it will do to the credibility of monetary and fiscal policy frameworks.

David Merkel has updated the inflation expectations implied by US Treasuries, noting that ‘rapidly rising long-term inflation expectations indicate that the average investor does not trust monetary policy to succeed over the next 20+ years’. At the same time, Merkel argues that since this outcome is already priced, it may be time to short US Treasury Inflation Protected Securities (TIPS). The US Treasury may well be taking the inflation nutters for a ride:

there is a lot of demand for long TIPS. If the US Treasury thinks it can get things under control, the rational thing to do is to stuff the long TIPS buyers with as much product as they can gulp before it becomes obvious that low inflation will continue because the government will soon balance the budget and pay down debt, as they did after WWII.

But Merkel also concedes that:

I don’t know which direction the US Government and Fed intend to go with policy. They likely have no idea as well…if the US Treasury can’t get things under control, the long TIPS buyers will do well, as they have the most sensitivity to rising forward inflation expectations.

The enormous uncertainty created by the discretionary policy responses of governments to the crisis will weigh on economic activity, regardless of how these issues are ultimately resolved.

posted on 20 January 2010 by skirchner in Economics, Financial Markets, Fiscal Policy, Monetary Policy

(0) Comments | Permalink | Main

The TD Securities – Melbourne Institute Monthly Inflation Gauge rose by 0.3% in December, following a 0.3% rise in November. In the twelve months to December, the Inflation Gauge rose by 2.6%. This is a fairly rapid acceleration from the October low of 1.2% y/y, which may well have been a turning point for CPI inflation. According to the Melbourne Institute, the gauge points to an increase in the December quarter CPI of 0.1%, yielding an annual inflation rate of 1.7%, a pick-up on the 1.3% annual rate seen in the September quarter. The December quarter CPI is released on 27 January.

posted on 18 January 2010 by skirchner in CPI, Economics, Financial Markets, Monetary Policy

(0) Comments | Permalink | Main

Follow the ETF money:

Some ETF investors appear to be positioning hedging against a continually rising dollar in 2010, based on the surging popularity of PowerShares DB U.S. Dollar Index Bullish Fund (UUP), which holds nearly $3 billion in assets.

The fund follows the movement of the U.S. dollar against a basket of six major currencies: the euro, the Japanese yen, the British pound, the Canadian dollar, the Swedish krona and the Swiss franc. As its name suggests, the ETF profits when the dollar strengthens against global currencies.

The fund has been such a hot seller that, twice in late 2009, it was forced to halt the creation of new shares when it ran out and awaited regulatory clearance to issue more shares.

Its mirror image, the PowerShares DB U.S. Dollar Index Bearish Fund (UDN), is geared to make money from a weakening dollar. It is much smaller with just under $300 million in total assets.

posted on 13 January 2010 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Justin Fox tells me that the UK-Australian edition of his The Myth of the Rational Market is out this month. My review of the US edition can be found over the fold.

continue reading

posted on 12 January 2010 by skirchner in Economics, Financial Markets

(5) Comments | Permalink | Main

The technology driving oil production.

posted on 12 January 2010 by skirchner in Economics, Oil

(1) Comments | Permalink | Main

Contracts on the monthly US unemployment rate make a welcome return at Intrade. There was a time when Intrade offered contracts on all US economic data releases, including non-farm payrolls, but the market-makers gave up on these contracts due to an insufficient number of noise traders. Economic derivatives markets have a poor track record of success in the US, with the CME shutting down its economic derivatives in 2007.

Perhaps the most successful economic derivatives market is iPredict in New Zealand, which also offers contracts on Australian economic data and the RBA’s official cash rate.

posted on 11 January 2010 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Jeremy Siegel still likes equities:

All indications are that the world economy has successfully dodged the depression bullet, and I believe economic activity will surprise on the upside. This means stronger than expected stock returns and weaker than expected bond returns.

While Jim Chanos is shorting China:

Mr. Chanos declined to be interviewed, citing his continuing research on China. But he has already been spreading the view that the China miracle is blinding investors to the risk that the country is producing far too much.

“The Chinese,” he warned in an interview in November with Politico.com, “are in danger of producing huge quantities of goods and products that they will be unable to sell.”

posted on 09 January 2010 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

An article in the Eastern Economics Journal ranks economics bloggers according to their scholarly impact. This blog is ranked 78th.

posted on 08 January 2010 by skirchner in Economics

(0) Comments | Permalink | Main

Macro Man’s non-predictions for 2010, here and here. MM’s 2009 performance is scored here.

posted on 08 January 2010 by skirchner in Economics, Financial Markets

(2) Comments | Permalink | Main

Reporting on Fed Chair Ben Bernanke’s speech to the American Economic Association has focused on his suggestion that ‘we must remain open to using monetary policy as a supplementary tool for addressing those risks’ associated with asset price inflation. However, the rest of his speech makes clear that Bernanke views this as very much a second-best option. His speech contains a review of the evidence against the notion that monetary policy was the main cause of the housing ‘bubble’ in the US and elsewhere.

The WSJ quotes Dale Jorgenson on what was missing from Bernanke’s speech:

a Harvard professor who served as Mr Bernanke’s thesis adviser at MIT in the 1970s, said the Fed chairman made a “pretty convincing” argument that low rates were not the driving force of the housing bubble.

But he said Mr Bernanke should have laid more blame at the feet of Congress for encouraging reckless mortgage lending with its support of Fannie Mae and Freddie Mac and other policies meant to increase home ownership.

“I didn’t hear any word with regard to going back to Congress about changing housing policy,” he said.

Leaving aside that fact that his reconfirmation is pending before Congress, one suspects that Bernanke knows a lost cause when he sees one. As the WSJ notes in another article:

In today’s Washington, we suppose, it only makes sense that the companies that did the most to cause the meltdown are being kept alive to lose even more money. The politicians have used the panic as an excuse to reform everything but themselves.

posted on 04 January 2010 by skirchner in Economics, Financial Markets, House Prices, Monetary Policy

(0) Comments | Permalink | Main

The WSJ examines the idea that economists are chronic cheapskates, citing both survey and anecdotal evidence. Given that economics proceeds from the notion of opportunity cost, this reputation is not hard to explain. The relative reluctance of economists to donate to charity may not be motivated by a lack of philanthropy, but by a better understanding of incentives or the unintended consequences of such generosity.

According to the WSJ:

Stanford University economist Robert Hall, incoming president of the American Economic Association, values his time so highly that his wife, economist Susan Woodward, occasionally puts her foot down. “Bob doesn’t see why we can’t just hire people to trim the Christmas tree,” she says. “I tell him that’s not what it’s supposed to be about.”

Hall has probably realised that the only genuinely scarce resource is the amount of attention an individual has to devote to their life-time activities. Shirley Conran had the same idea when she declared that life was too short to stuff a mushroom.

posted on 02 January 2010 by skirchner in Economics

(1) Comments | Permalink | Main

Peter Wallison on the biggest public policy disaster in US history.

Henry Ergas on the unacknowledged efficiency costs of an ETS.

The welfare costs of government playing Santa.

posted on 01 January 2010 by skirchner in Economics

(0) Comments | Permalink | Main

|