2008 11

Roger Howard, author of The Oil Hunters, on how foreign oil creates interdependence rather than dependence:

to identify America’s “foreign oil dependency” as a source of vulnerability and weakness is just too neat and easy.

This identification wholly ignores the dependency of foreign oil producers on their consumers, above all on the world’s largest single market—the United States. Despite efforts to diversify their economies, all of the world’s key exporters are highly dependent on oil’s proceeds and have always lived in fear of the moment that has now become real—when global demand slackens and prices fall. The recent, dramatic fall in price per barrel—now standing at around $54, less than four months after peaking at $147—perfectly exemplifies the producers’ predicament.

So even if such a move were possible in today’s global market, no oil exporter is ever in a position to alienate its customers. Supposed threats of embargoes ring hollow because no producer can assume that its own economy will be damaged any less than that of any importing country. What’s more, a supply disruption would always seriously damp global demand. Even in the best of times, a prolonged price spike could easily tip the world into economic recession, prompt consumers to shake off their gasoline dependency, or accelerate a scientific drive to find alternative fuels. Fearful of this “demand destruction” when crude prices soared so spectacularly in the summer, the Saudis pledged to pump their wells at full tilt. It seems that their worst fears were realized: Americans drove 9.6 billion fewer miles in July this year compared with last, according to the Department of Transportation.

Instead, the dependency of foreign oil producers on their customers plays straight into America’s strategic hands.

posted on 29 November 2008 by skirchner in Economics, Oil

(0) Comments | Permalink | Main

Rory Robertson gets ready to send Steve Keen on a long walk:

To make it interesting, I offered Dr Keen a challenge…

On the maybe 1% chance that he is right, and capital-city home prices do indeed fall by 40% within the next five years - starting from Q2 2008, and as measured by the ABS - I will walk from Canberra to the top of Mt Kosciusko (that’s maybe 200km followed by a 2228-metre incline).

If Dr Keen turns out to be less than half right, as I expect, and home prices drop by (much) less than 20%, he will take that long walk. Moreover, the loser must wear a tee-shirt saying: “I was hopelessly wrong on home prices! Ask me how.”

We now have a bet, and I expect to record an easy win within two years.

posted on 28 November 2008 by skirchner in Economics

(3) Comments | Permalink | Main

The Centre for Independent Studies has released my Policy Monograph Capital Xenophobia II: Foreign Direct Investment in Australia, Sovereign Wealth Funds and the Rise of State Capitalism.

The monograph revisits the subject of Wolfgang Kasper’s original 1984 Capital Xenophobia monograph. Wolfgang was kind enough to write the foreword to this update of his earlier work on the subject.

There is an op-ed version in today’s AFR for those who have access, reproduced below the fold for those who don’t (text may differ slightly from the edited AFR version).

continue reading

posted on 27 November 2008 by skirchner in Economics, Financial Markets

(1) Comments | Permalink | Main

Larry White has a new Cato Briefing Paper How Did We Get into This Financial Mess? White echoes a now widespread criticism of US monetary policy, that is was too easy in the first half of this decade:

The federal funds rate began 2001 at 6.25 percent and ended the year at 1.75 percent. It was reduced further in 2002 and 2003, inmid-2003 reaching a record low of 1 percent, where it stayed for a year. The real Fed funds rate was negative - meaning that nominal rates were lower than the contemporary rate of inflation - for two and a half years.

White also notes that the Fed funds rate was below that implied by the Taylor rule, a point that Taylor himself has also made.

That US monetary policy was easy at this time was no accident. It was a very deliberate policy choice on the part of the FOMC. Why was policy kept so easy for so long? One reason was the perceived threat of deflation, as Vince Reinhart recalls:

According to FOMC meeting transcripts from that year, then Chairman Alan Greenspan in November [2002] called deflation “a pretty scary prospect, and one that we certainly want to avoid.”

Then Gov. Ben Bernanke, now Fed chairman, said in September 2002, “the strategy of preemptive strikes should apply with at least as great a force to incipient deflation as it does to incipient inflation.”

In hindsight while there was clearly a strong disinflation trend back then, outright deflation didn’t appear to be as big a risk as the Fed thought. Annual growth in consumer prices never fell below 1% and was rarely below 2% after 2002.

The problem back then, Reinhart said, was “we didn’t know why inflation was going down as much as it was.”

That year, 2002, “was very much a story of uncertainty about the inflation process with some modest identifiable forces putting downward pressure” on prices, he said.

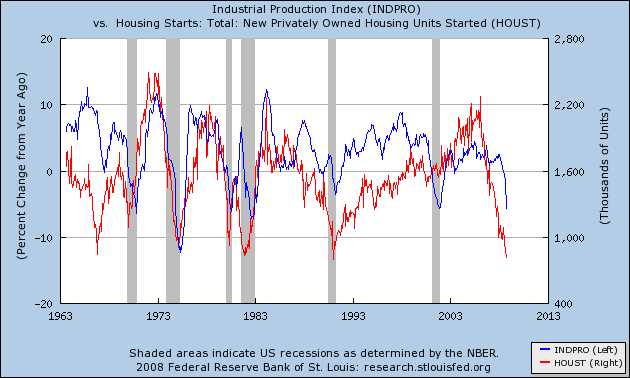

This puts the failure of US monetary policy to respond to the emerging US housing boom in its proper context. The following chart shows annual growth in US industrial production as a proxy for the broader economy, along with new privately-owned dwelling starts as a proxy for housing activity. Shaded bars are NBER-defined recessions.

The 2001 recession was exceptional compared to previous business cycles, in that housing activity did not see a significant downturn along the rest of the US economy. Industrial production was subdued coming out of the 2001 recession (note the double dip into negative growth), while housing continued to enjoy a strong expansion. If the 2001 recession could not tame the US housing boom, then it is hard to see how tighter US monetary policy could have done so without inflicting significant, and potentially deflationary, collateral damage on the rest of the economy.

One could argue that Fed policy was a success on its own terms, because it achieved exactly what it set out to do: pre-empt the threat of deflation.

posted on 21 November 2008 by skirchner in Economics, Financial Markets

(35) Comments | Permalink | Main

RBA Governor Glenn Stevens’ speech to CEDA last night has been widely interpreted as giving a ‘green light’ to deficit spending, as if politicians ever needed permission or encouragement from the Reserve Bank to ramp-up spending. The really significant part of Stevens’ speech went largely unnoticed:

in addition to the many useful steps being planned by regulators, perhaps we could pay more attention to the low-frequency swings in asset prices and leverage (even if that means less attempt to fine-tune short-period swings in the real economy); we could have a more conservative attitude to debt build-up; and we could exhibit a little more scepticism about the trade-off between risks and rewards in rapid financial innovation. This would constitute a useful mindset for us all to take from this episode.

The fudge word here, of course, is ‘more.’ More could simply mean giving greater weight to the implications of developments in asset prices for inflation and the overall economy. However, it could potentially extend much further, to an attempt by central bankers to actively manage asset prices at the expense, as Stevens suggests, of shorter-run demand management. As I argue here, the historical precedents for this are far from encouraging.

A more recent example of a central bank conditioning monetary policy on asset prices was the Reserve Bank of New Zealand’s use of the trade-weighted exchange rate as part of a composite operating target between 1996 and 1999, known as the monetary conditions index. This practice was abandoned, because the well-known volatility of exchange rates and their very loose relationship with economic fundamentals made it a very poor basis for conducting monetary policy. The weaker the connection between asset prices and economic fundamentals, the stronger the argument against using asset prices as either targets or conditioning variables for monetary policy.

posted on 20 November 2008 by skirchner in Economics, Financial Markets

(7) Comments | Permalink | Main

The software that runs Institutional Economics has been updated. Please let me know if you experience any problems: info at institutional-economics.com. This site is powered by ExpressionEngine.

posted on 15 November 2008 by skirchner in Misc

(0) Comments | Permalink | Main

The federal government is proposing to further regulate credit ratings agencies:

The Government also unveiled changes to the regulation of credit ratings agencies that will require them to hold an Australian Financial Services Licence and to report annually on the quality and integrity of their ratings processes.

The changes reflect a growing demand in the global investment community for greater oversight of ratings agencies, which have become the target of criticism, particularly for their role in rating structured finance.

This ignores the somewhat inconvenient truth that the role of ratings agencies in credit markets was itself mandated by regulation. As Charles Calomiris has argued, the regulatory power given to the ratings agencies encouraged them to compete on relaxing the cost of regulation to investors, generating huge fees for the ratings agencies in the process. Calomiris summed it up this way: ‘the regulatory use of ratings changed the constituency demanding a rating from free-market investors interested in a conservative opinion to regulated investors looking for an inflated one.’ Calomiris notes that both Congress and the SEC actually encouraged ratings inflation in relation to sub-prime CDOs, an unintended consequence of their promotion of rules designed to prevent ‘anti-competitive’ behaviour on the part of the dominant ratings agencies.

posted on 14 November 2008 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

I have an op-ed in today’s Australian, arguing against the view that central banks should explicitly target asset prices:

In 2002, prior to becoming Fed chairman, Bernanke gave a speech titled Asset “Bubbles” and Monetary Policy. Bernanke noted that “the correct interpretation of the 1920s is not the popular one: that the stock market got overvalued, crashed and caused a Great Depression. The true story is that monetary policy tried overzealously to stop the rise in stock prices. But the main effect of the tight monetary policy was to slow the economy. The slowing economy, together with rising interest rates, was in turn a major factor in precipitating the stock market crash”.

The singular cause of the Great Depression of the 1930s, in Bernanke’s view, was that the Federal Reserve fell under “the control of a coterie of bubble poppers”.

Bernanke was merely reaffirming a well-established consensus among economists, ranging all the way from John Maynard Keynes to Milton Friedman. In his A Treatise on Money, Keynes said: “I attribute the slump of 1930 primarily to the deterrent effects on investment of the long period of dear money which preceded the stock market collapse and only secondarily to the collapse itself.” Friedman’s 1963 A Monetary History of the United States also laid blame for the Great Depression squarely at the feet of the Fed and its attempt to become “an arbiter of security speculation or values”.

posted on 12 November 2008 by skirchner in Economics, Financial Markets

(10) Comments | Permalink | Main

I have an op-ed in today’s SMH critical of the federal government’s ‘new’ car industry plan:

Labor’s manufacturing fetish is long-standing and deeply held. Kevin Rudd’s observation, made as opposition leader in 2006, that he wanted Australia to be “more than a mine for China and a beach for the Japanese” suggests this fetish is based on a caricature of the Australian economy…

The billions of dollars in help provided by successive Australian governments to the local car industry has come at the expense of consumers and taxpayers, destroying jobs and income in other industries. This is the real, but largely unseen, cost of industry assistance.

posted on 11 November 2008 by skirchner in Economics

(0) Comments | Permalink | Main

The scapegoating of Alan Greenspan across the political spectrum has been shameful and shameless. It is therefore pleasing to see that the Cato Institute has published a timely defence of Greenspan by David Henderson and Jeff Rogers Hummel. Henderson and Hummel argue that:

Alan Greenspan stands out as the most competent—and arguably the only competent—helmsman of United States monetary policy since the creation of the Federal Reserve System…

his policy may have ended up slightly too discretionary. But that possibility hardly justifies the “asset bubble” hubris of those economic prognosticators who, only well after the fact, declaim with absolutely certainty and scant attention to the monetary measures, how the Fed could have pricked or prevented such bubbles…

Rather than demonstrating that monetarist rules are obsolete and free banking unnecessary, Greenspan’s policies suggest that the more thoroughly either of those two objectives is implemented, the greater the macroeconomic stability our economy will enjoy.

I made a similar argument here about how contemporary central banking closely approximates the free banking ideal of a market-determined monetary order.

posted on 10 November 2008 by skirchner in Economics, Financial Markets

(1) Comments | Permalink | Main

ABC Learning Chair Sallyanne Atkinson learns political economy the hard way:

DEEP in debt, Sallyanne Atkinson appears stunned by the collapse of ABC Learning.

“I find that absolutely bizarre” the businesswoman who chaired the failed childcare corporation for seven years said yesterday when told 40 per cent of the centres are unprofitable.

“This is a business subsidised by the Government. How can it be unprofitable?”

posted on 09 November 2008 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Former Australian Treasurer Peter Costello once told us that the G20 was ‘important in itself,’ an idea to which he could easily relate. Former IMF Chief Economist Simon Johnson continues this fine tradition of explaining the relevance of the G20:

the fact that G20 heads of government will now start meeting (dinner is on November 14; mark your calendars) is most significant. Almost always, once a group like this meets, it can agree on its own importance and the need for another meeting.

I’m sure we can all sleep a little easier at night, knowing the G20 is on the job.

posted on 09 November 2008 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

Ray Fair’s final US Presidential election equation update:

The final economic values (‘final’ as of October 30, 2008) are 0.22 for GROWTH, 2.88 for INFLATION, and 3 for GOODNEWS. Given these values, the predicted Republican vote share (of the two-party vote) is 48.09 percent. So the prediction is 51.91 for the Democrats and 48.09 for the Republicans, for a spread of 3.82.

The current situation is unusual in that the economy since the end of the third quarter appears to have gotten much worse. People may perceive the economy to be worse than the economic values through the third quarter indicate, which, other things being equal, suggests that the vote equation may overpredict the Republican share. But for what it is worth, the final vote prediction is 48.09 percent of the two-party vote for the Republicans. The Republican share of the two-party House vote is predicted to be 44.24 percent.

posted on 01 November 2008 by skirchner in Economics, Financial Markets

(0) Comments | Permalink | Main

|