What Did They Know and When Did They Know It: Ex-Ante Views on US Housing

Looking through all the after-the-fact wisdom and hand-wringing, a Boston Fed discussion paper examines the ex ante views of economists in relation to the US housing market:

From our review of the pre-crisis housing literature from the early-to-mid-2000s, it is apparent that well-trained and well-respected economists with the best of motives could and did look at the same data and come to vastly different conclusions about the future trajectory of U.S. housing prices. This is not such a surprising observation once one realizes that the state-of-the-art tools of economic science were not capable of predicting with any degree of certainty the collapse of U.S. house prices that started in 2006.

The paper has mostly fatal implications for the idea that the authorities can actively manage cycles in house prices.

posted on 17 August 2010 by skirchner in Economics, Financial Markets, House Prices

(0) Comments | Permalink | Main

Did Cheap Credit Fuel the US Housing Boom?

No, according to Ed Glaeser and his co-authors:

Interest rates do influence house prices, but they cannot provide anything close to a complete explanation of the great housing market gyrations between 1996 and 2010. Over the long 1996-2006 boom, they cannot account for more than one-fifth of the rise in house prices. Their biggest predictive influence is during the 2000-2005 period, when long rates fell by almost 200 basis points. That can account for about 45% of the run-up in home values nationally during that half-decade span. However, if one is going to cherry-pick time periods, it also must be noted that falling real rates during the 2006-2008 price bust simply cannot account for the 10% decline in FHFA indexes those years. There is no convincing evidence from the data that approval rates or down payment requirements can explain most or all of the movement in house prices either.

The authors also note that Robert Shiller’s ‘irrational exuberance’ is a non-explanation:

even if Case and Shiller are correct, and over-optimism was critical, this merely pushes the puzzle back a step. Why were buyers so overly optimistic about prices? Why did that optimism show up during the early years of the past decade and why did it show up in some markets but not others? Irrational expectations are clearly not exogenous, so what explains them? This seems like a pressing topic for future research. Moreover, since we do not understand the process that creates and sustains irrational beliefs, we cannot be confident that a different interest rate policy wouldn’t have stopped the bubble at some earlier stage. It is certainly conceivable that a sharp rise in interest rates in 2004 would have let the air out of the bubble. But this is mere speculation that only highlights the need for further research focusing on the interplay between bubbles, beliefs and credit market conditions.

A more fruitful line of inquiry would be to investigate fundamental factors such as the role of US housing GSEs in distorting the allocation of global capital.

posted on 04 August 2010 by skirchner in Economics, Financial Markets, House Prices, Monetary Policy

(0) Comments | Permalink | Main

Yet Another New Tax on NSW Housing

The NSW government has introduced yet another new tax on housing transactions. Yesterday, I gave a post-budget presentation to a business group in Western Sydney, together with Westpac’s Matthew Hassan. Matthew presented some stunning charts showing the growth in the tax burden on housing in each state, with NSW the clear winner. Indeed, the tax burden on a new house and land package on Sydney’s suburban fringe is now such as to make it unprofitable to bring to market, which helps explain why new housing supply in the state is running at 1950s levels.

If only some of the outrage directed against negative gearing and capital gains tax concessions by ignorant journalists and commentators could be marshalled against the taxes and charges that are really responsible for putting upward pressure on house prices.

posted on 13 May 2010 by skirchner in Economics, House Prices

(4) Comments | Permalink | Main

The US Housing ‘Bubble’ that Wasn’t

Some refreshing ‘bubble’ scepticism from Casey Mulligan:

Adjusted for inflation, residential property values were still higher at the end of 2009 than 10 years ago. This fact raises the possibility that at least part of the housing boom was an efficient response to market fundamentals.

posted on 07 May 2010 by skirchner in Economics, House Prices

(0) Comments | Permalink | Main

The Market Believes the RBA is Targeting House Prices

The weighted average of capital city established house prices rose a Steve Keen-busting 4.8% q/q and 20% y/y for the March quarter, with gains in Sydney and Melbourne in excess of 20% y/y. This saw three-year bond futures savaged by around 7 basis points and the implied probability of a 25 basis points tightening from the RBA tomorrow surge from around 50% to around 65% on iPredict. The ugly 3.4% annualised result for the trimmed mean of the TD-MI inflation gauge released an hour earlier should be more important for the RBA’s deliberations, but it is house prices that are grabbing the market’s attention.

posted on 03 May 2010 by skirchner in Economics, Financial Markets, House Prices, Monetary Policy

(1) Comments | Permalink | Main

The Fix is In

In a previous post, I warned that:

The danger now is that the government implements another of its short-term political fixes ahead of this year’s federal election and re-tightens the rules [on foreign direct investment in residential property] rather than addressing the supply-side constraints besetting Australian residential property.

In the event, we have this:

FEDERAL and state governments have commissioned a working party of officials to hold a no-stone-unturned inquiry into all factors contributing to record house prices, as Labor senses the issue is becoming a political danger.

The inquiry, to deliver its first report within weeks, will examine sensitive areas such as tax breaks for negative gearing, land banking by developers, and whether grants to first home buyers push up house prices.

More wide-ranging than I expected, but also a waste of time, something the government is fast running out of ahead of this year’s federal election. As Christopher Joye notes, these issues have already been extensively studied and the policy solutions are well-known. The likely outcome is a short-term political fix designed to serve as a holding action ahead of the election. Do we really need an inquiry into whether grants to first home buyers push up house prices? Even Steve Keen and I agree on that. Did we really need a review by a former senior public servant to tell us that the home insulation program was a waste?

While the Prime Minister has an underserved reputation as a policy wonk, the reality is that he is what former Prime Minister Paul Keating would call a ‘policy bum’.

posted on 23 April 2010 by skirchner in Economics, House Prices

(4) Comments | Permalink | Main

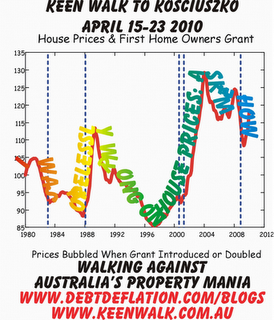

True Confessions of Steve Keen on the Road to Mt. Kosciuszko

The Business Spectator’s Rob Burgess, who has joined Steve Keen’s housing doomsday cult, reveals the real story behind Keen’s highly publicised decision to sell his unit in Surry Hills:

It turns out that Steve has a cunning get-rich-quick plan. In late 2008, just after Lehman Brothers crashed and a month after he’d made the house-price bet with Rory Robertson, Keen sold his house, taking large capital gains out of the market. Now, if he can only crash the housing market, he’ll make a killing! (Cue fiendish laughter from evil Dr Keen.)

It is, of course, absurd to think that even a cash-strapped academic would manipulate the market to extract relatively small sums of money (in fact, says Keen, the sale was divorce-related).

posted on 20 April 2010 by skirchner in Economics, House Prices

(0) Comments | Permalink | Main

Sticking it Up the Wrong People

Steve Keen’s housing doomsday cult is wending its way up Mt Kosciuszko with an ETA of 23 April. By my count, only ten people turned up to see him off from Canberra, but Keen is quoted as saying:

’‘This has actually garnered me support,’’ he said. ‘‘People are saying, thank god someone is sticking it up the property industry.’‘

A theme of Keen’s housing doomsday cult is that hapless home buyers are being manipulated into buying property, resulting in a ‘housing mania.’ Like many of his fellow travelers, Keen sees housing affordability as a demand-side rather than a supply-side problem.

Yet it should be obvious that it is in the interests of the property industry to promote housing affordability so that it can sell more houses. The industry’s lobby groups and industry associations consistently argue for an easing of the tax burden on housing, development restrictions and other supply-side constraints on the provision of new homes. The property industry’s interest in building and selling more homes is aligned with the consumer interest in making housing more affordable. Keen is sticking it to the wrong people. Like any industry, it has its share of spruikers and shonks, but the property industry in general is the solution and not the problem.

posted on 17 April 2010 by skirchner in Economics, House Prices

(9) Comments | Permalink | Main

Data are the More than Just the Plural of Anecdote

The debate over foreign investment in Australian property is being fuelled by anecdote rather than data, largely because the available data on the subject is so limited. In today’s Australian, Natasha Bita reports her experiences trying to extract information from the FIRB (an all too familiar story):

The Australian provided the FIRB with a list of questions, including whether it is monitoring the impact on the property market of its relaxed rules, which richocheted for three days between FIRB and the Treasury.

Eventually, a spokesman for Sherry failed to say if, or how, the impact was being monitored.

A request for a copy of FIRB’s advice to Treasury to change the foreign investment rules also was ignored.

Asked to provide up-to-date data on the sale of residential property to foreigners and temporary residents, the minister’s spokesman replied: “FIRB approvals for temporary residents to buy established houses as a percentage of the total number of transfers of established housing that occurred in the eight capital cities were at a level of approximately between 1.5 per cent and 2 per cent in recent times. Data are not available after 31 March 2009 given that temporary residents were exempted from FIRB notification requirements.”

Even the Reserve Bank, which claims to be monitoring the situation, is having trouble getting any meaningful data from FIRB.

Its only analysis is a two-page internal briefing note, based on statistics from FIRB’s 2007-08 annual report and temporary resident numbers.

“For analysis you would try to get hard data on this but there is in fact no hard data,” the Reserve Bank’s head of domestic markets, John Broadbent, says.

“The Treasury were the ones who decided to cease collecting some of the data sets on the basis they were looking to reduce the administrative burden.”

Broadbent says an analysis of “older data” from the FIRB shows the share of foreign buyers of residential properties has risen from 0.4 per cent of properties in the late 90s to 1 per cent in 2008.

This is a very good illustration of how the FIRB’s lack of transparency undermines support for foreign investment in Australia. The publication of more detailed and timely data on the subject would go a long way to dispelling popular fears about foreign investment. That said, I also have some sympathy for the Treasury position. It is unrealistic to expect FIRB to monitor and enforce compliance with the rules in relation to thousands of property transactions. Indeed, it is doubtful whether FIRB even has the resources to monitor compliance with the many conditions it has been piling on to some of the more high profile cross-border M&A transactions. The government’s appetite for regulation in this area greatly exceeds its administrative capacity. Much of the liberalisation of foreign investment rules undertaken by the Rudd government has been an attempt to ease the administrative burden on the FIRB.

If the anecdotes are to be believed, then the liberalisation of foreign investment rules in relation to property has been a success. If there is a policy failure, it is in the inability of the supply-side of the market to respond flexibly to both foreign and domestic demand. The danger now is that the government implements another of its short-term political fixes ahead of this year’s federal election and re-tightens the rules rather than addressing the supply-side constraints besetting Australian residential property.

posted on 12 April 2010 by skirchner in Economics, Foreign Investment, House Prices

(0) Comments | Permalink | Main

Steve Keen Hides His Shame

Steve Keen’s design for a t-shirt to wear on the march of his housing doomsday cult to the top of Mount Kosciuszko looks like a CAPTCHA challenge-response test:

As Chris Joye notes, the proposed design ‘directly dishonours the agreement he struck with Macquarie Bank’s Rory Robertson’ to wear a t-shirt that read ‘I was hopelessly wrong on house prices. Ask me how’.

posted on 13 March 2010 by skirchner in Economics, Financial Markets, House Prices

(1) Comments | Permalink | Main

Steve Keen’s Latest Media Stunt

In an attempt to snatch victory from the jaws of defeat in his wager with Rory Robertson, Steve Keen seeks to lead a lemming-like march of housing doomers up the slopes of Mt. Kosciuszko:

rather than accept the victory of his more bullish opponent, it appears the professor is trying to muster the biggest gathering of market bears in Australian economic history. He has already coined the event ‘‘Walking Against Australia’s Property Mania.’’

Keen will start his 224-kilometre walk from Parliament House in Canberra on April 15, and aside from a documentary crew, his girlfriend and a masseuse, he hopes to be accompanied by some of the 3000-odd members of his Debtwatch blog.

The other side of the bet is unimpressed:

“Betting the house on an economist’s forecast typically is not a smart move. Unfortunately, Dr Keen recklessly encouraged everyday Australians to sell their homes at what turned out to be the peak of the global financial crisis, and the trough in local house prices,” Rory Robertson responded.

“That’s why he’s getting set to walk from Canberra to Mt Kosciuszko wearing a t-shirt saying, ‘I was hopelessly wrong on house prices. Ask me how!’”

posted on 16 February 2010 by skirchner in Economics, House Prices

(4) Comments | Permalink | Main

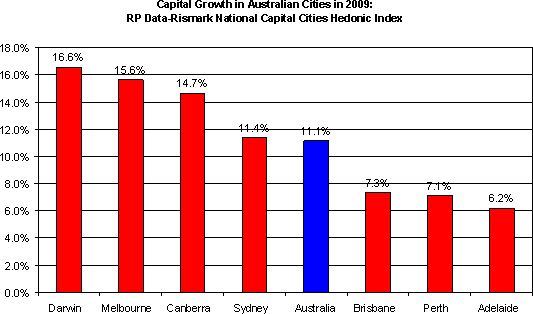

Australian House Prices Post 11% Gain in 2009

The RP Data-Rismark national capital city hedonic home price index for December shows a modest fall of 0.3% for the month, but up 2.1% for the quarter and 11.1% for the calendar year. This follows modest declines of 2-3% in 2008, which was the worst performance in history on this measure.

posted on 29 January 2010 by skirchner in Economics, House Prices

(0) Comments | Permalink | Main

Steve Keen They Hardly Knew You: Consumer House Price Expectations

The January Westpac-Melbourne Institute Consumer Sentiment survey finds that 84% expect house prices to increase over the next 12 months, with 21% expecting gains of over 10%.

posted on 23 January 2010 by skirchner in Economics, House Prices

(14) Comments | Permalink | Main

Bernanke on Monetary Policy and the Housing ‘Bubble’

Reporting on Fed Chair Ben Bernanke’s speech to the American Economic Association has focused on his suggestion that ‘we must remain open to using monetary policy as a supplementary tool for addressing those risks’ associated with asset price inflation. However, the rest of his speech makes clear that Bernanke views this as very much a second-best option. His speech contains a review of the evidence against the notion that monetary policy was the main cause of the housing ‘bubble’ in the US and elsewhere.

The WSJ quotes Dale Jorgenson on what was missing from Bernanke’s speech:

a Harvard professor who served as Mr Bernanke’s thesis adviser at MIT in the 1970s, said the Fed chairman made a “pretty convincing” argument that low rates were not the driving force of the housing bubble.

But he said Mr Bernanke should have laid more blame at the feet of Congress for encouraging reckless mortgage lending with its support of Fannie Mae and Freddie Mac and other policies meant to increase home ownership.

“I didn’t hear any word with regard to going back to Congress about changing housing policy,” he said.

Leaving aside that fact that his reconfirmation is pending before Congress, one suspects that Bernanke knows a lost cause when he sees one. As the WSJ notes in another article:

In today’s Washington, we suppose, it only makes sense that the companies that did the most to cause the meltdown are being kept alive to lose even more money. The politicians have used the panic as an excuse to reform everything but themselves.

posted on 04 January 2010 by skirchner in Economics, Financial Markets, House Prices, Monetary Policy

(0) Comments | Permalink | Main

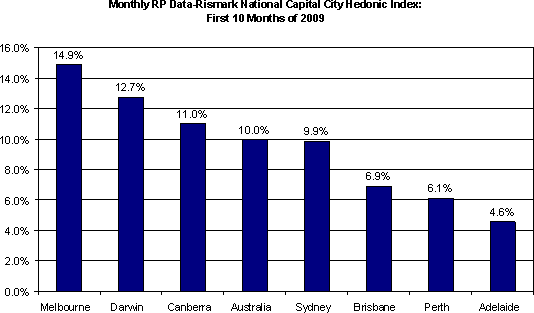

Australian House Prices Up 10% YTD

RP Data-Rismark have released the capital city hedonic house price index for October, showing house prices up 10% YTD.

Here’s what $1.85 million buys you in the Sydney suburb of Paddington:

posted on 30 November 2009 by skirchner in Economics, House Prices

(1) Comments | Permalink | Main

Page 2 of 3 pages < 1 2 3 >

|